The objective of this article is to evaluate different techniques for time series forecasting. These techniques include OLS model, Co-integration model and ARIMAX model

Business problem: To forecast the different components of PPNR. These components include Non-interest Income and Non-interest Expense.

Proposed solution

OLSModel

Co-IntModel

ARIMAXModel

Notes

Preference

High

Medium

Low

Complexity

Low

Medium

High

Dependent variable is stationary

OLS should be used

ARIMAX should be used

For ARIMAX both (dependent and independent variables) should be stationary together

Independent variable is stationary

Dependent variable is non-stationary

Co-Int should be used

ARIMAX should be used

For ARIMAX both (dependent and independent variables) should be non-stationary together

Independent variable is non-stationary

Auto-correlation

DW test close to 2

DW test close to 2

DW test close to 2

If for OLS or Co-integration DW fails then ARIMAX should be used

Variable significance

p-value < 0.05

p-value < 0.05

p-value < 0.05

For ARIMAX the AR, MA and exogenous terms should be significant

Multi co-linearity

VIF < 5

VIF < 5

VIF < 5

Residual is stationary

ADF test should pass

ADF test should pass

ADF test should pass

Residual is non-stationary

For all the three approaches, the residual should be stationary

Normality and homoscedasticity of residual

Should pass

Should pass

Should pass

OLS

Advantages – easy to develop / test and easy to explain

Disadvantages– difficult to finding strong correlation between dependent and independent variables

Co-Integration

Advantages – easy to find strong correlations between dependent and independent variables

Disadvantages – difficult to pass all the tests / assumptions of co-integration

ARIMAX

Advantages – very powerful modeling technique to overcome the shortcomings of OLS and co-integration models

Disadvantages – complex to develop as there are two stages. In stage 1 OLS model is developed and in stage 2 ARIMAX model is developed post identification of AR and MA terms

Introduction

PPNR

Pre-provision net revenue (PPNR), under the Federal Reserve’s Comprehensive Capital Analysis and Review (CCAR), measures net revenue forecast from asset-liability spreads and non-trading fees of banks.

Pre-provision Net Revenue (PPNR) = Net Interest Income + Non-interest Income – Non-interest Expense

Interest Income: Loans and Securities

Interest Expense: Deposits and Bonds

Non-Interest Income: Credit Related Fees and Non-Credit Related

If the dependent and independent variables are stationary

ADF test is done on the independent variables. Only those variables are kept, those are stationary.

Correlation between independent variables and dependent variable is done. Only those variables are kept, those have high correlation with dependent variable.

OLS Model is developed.

If the dependent and independent variables are non-stationary

ADF test is done on the independent variables. Only those variables are kept, those are non-stationary

Co-integration between independent variables and dependent variable is done. Only those variables are kept, those are co-integrated with dependent variable.

Correlation between independent variables and dependent variable is done. Only those variables are kept, those have high correlation with dependent variable.

OLS Model is developed

2.3 Independent Variables

Raw

Diff QoQ

Diff YoY

Pct Diff QoQ

Pct Diff YoY

Lags 0, 1 and 2

Lags 0, 1 and 2

Lags 0, 1 and 2

Lags 0, 1 and 2

Lags 0, 1 and 2

GDP growth

Yes

No

No

No

No

Income growth

Yes

No

No

No

No

CPI growth

Yes

No

No

No

No

Unemp rate

Yes

Yes

Yes

No

No

3mT rate

Yes

Yes

Yes

No

No

5yT rate

Yes

Yes

Yes

No

No

10yT rate

Yes

Yes

Yes

No

No

BBB rate

Yes

Yes

Yes

No

No

Prime rate

Yes

Yes

Yes

No

No

HPI

Yes

No

No

Yes

Yes

2.4 Model Outputs

Time Period

Historical – 44 data points (from 2005Q1 to 2015Q4)

Forecasted – 13 data points (from 2016Q1 to 2019Q1)

Non-interest Income and Non-interest Expense are modeled

Non-interest Expense is modeled using the stationary model developed approach

Non-interest Income is modeled using the non-stationary model developed approach

Non-interest Expense(Stationary model developed approach)

Non-interest Income(Non-stationary model developed approach)

2.5 Model Tests

Stationarity of dependent and independent variables:

ADF test is done

If the p-value <= 0.10 then the series is stationary

If the p-value > 0.10 then the series is non-stationary

Multi co-linearity:

Correlation matrix is used to test multi co-linearity

If the correlation between variables is less than 0.30 or more than -0.30 then there is low multi co-linearity

If the correlation between variables is more than 0.70 or less than -0.70 then there is high multi co-linearity

Significance:

The p-value <= 0.05 then the coefficient is statistically significant

The p-value > 0.05 then the coefficient is statistically insignificant

Auto correlation:

Durbin-Watson test is done

If DW statistics is less than 1 then there is positive auto correlation

If DW statistics is close to 2 then there is no auto correlation

If DW statistics is more than 3 then there is negative auto correlation

Stationarity of residual:

ADF test is done

If the p-value <= 0.10 then the series is stationary

If the p-value > 0.10 then the series is non-stationary

3. Stationary Series

3.1 Process

ADF test is done on the independent variables. Only stationary variables are kept (23 out of 72 variables are selected).

Correlation between independent variables and dependent variable is done. Only those variables are kept, that have high correlation with dependent variable (2 out of 23 variables are selected).

OLS Model is developed, checks on multi co-linearity, significance of the variable and stationary of the residuals are done (2 out of 2 variables are selected).

3.2 Dependent Variables

It is observed that the dependent variables (Non-Interest Income 1st Difference and Non-Interest Expense 1st Difference) are stationary

Non-Interest Income 1st Diff = Non-Interest Income (t) – Non-Interest Income (t-1)

It is observed that out of 72 independent variables, 23 independent variables are stationary.

If the p-value <= 0.10 then the series is stationary

If the p-value > 0.10 then the series is non-stationary

It is observed that no macro-economic variable has high correlation with Non-Interest Income 1st Diff. However, few macro-economic variables have high correlation with Non-Interest Expense 1st Diff.

If correlation is more than 0.30 or less than -0.30 then it is marked as high

It is observed that out of 23 independent variables, 2 independent variables have high correlation with Non-Interest Expense 1st Diff.

NonInt Exp diff

CPI growth

0.31

GDP growth 2

0.43

3.4 Model Development

It is observed that the model has low R-Sq and Adj R-Sq.

No. Obs:

43.00

R-squared:

0.29

Df Model:

2.00

Adj. R-squared:

0.26

There are 2 variables in the model.

CPI growth and GDP growth (lag 2)

The p-value for both the variables is less than 0.05

coef

std err

t

P>|t|

const

-377,300.00

134,000.00

-2.82

0.01

CPI growth

86,320.00

35,500.00

2.43

0.02

GDP growth 2

122,800.00

36,600.00

3.36

0.00

It is observed that there is very low multi co-linearity in the model

Correlation between variables is less than 0.30 or more than -0.30

CPI growth

GDP growth 2

CPI growth

-0.04

GDP growth 2

-0.04

It is observed that there is no auto-correlation in the model and the residual is stationary

DW test statistics is close to 2

The p-value of the ADF test is less than 0.10

Durbin-Watson:

2.36

Var:

ADF:

Pval:

RESI

-8.30

0.00

3.5 Projection

The projection is done for 13 Quarters

If t = 1: Predicted Non-Interest Expense (t) = Actual Non-Interest Expense (t)

If t > 1: Predicted Non-Interest Expense (t) = Predicted Non-Interest Expense (t-1) + Predicted Non-Interest Expense 1st Diff (t)

The severely adverse projection is done for forecasted period

4. Non-stationary Series

4.1 Process

ADF test is done on the independent variables. Only non-stationary variables are kept (49 out of 72 variables are selected).

Co-integration between independent variables and dependent variable is done. Only those variables are kept, those are co-integrated with dependent variable (6 out of 49 variables are selected).

OLS Model is developed, checks on multi co-linearity, significance of the variable and stationary of the residuals are done (1 out of 6 variables is selected).

4.2 Dependent Variables

It is observed that the dependent variables are non-stationary

Var

ADF

Pval

NonInt Inc

-2.14

0.23

NonInt Exp

-1.49

0.54

4.3 Independent Variables

It is observed that out of 72 independent variables, 49 independent variables are non-stationary.

If the p-value <= 0.10 then the series is stationary

If the p-value > 0.10 then the series is non-stationary

It is observed that no macro-economic variable is co-integrated with Non-Interest Expense. However, few macro-economic variables are co-integrated with Non-Interest Income.

If the p-value <= 0.10 then the series is co-integrated

If the p-value > 0.10 then the series is not co-integrated

Var

Coint_Inc

Pval_Inc

3mT rate dyoy

-3.37

0.05

3mT rate dyoy 1

-3.24

0.06

5yT rate dyoy

-3.21

0.07

5yT rate dyoy 1

-3.38

0.04

Prime rate dqoq 2

-3.39

0.04

Prime rate dyoy

-3.31

0.05

4.4 Model Development

It is observed that the model has high R-Sq and Adj R-Sq.

No. Obs:

44.00

R-squared:

0.66

Df Model:

1.00

Adj. R-squared:

0.65

There is 1 variable in the model.

3mT rate (difference YoY)

The p-value for the variable is less than 0.05

coef

std err

t

P>|t|

const

7,656,000.00

249,000.00

30.80

0.00

3mT rate dyoy

1,786,000.00

199,000.00

8.99

0.00

It is observed that there is positive auto-correlation in the model and the residual is stationary

DW test statistics is less than 1

The p-value of the ADF test is less than 0.10

Durbin-Watson:

0.85

Var:

ADF:

Pval:

RESI

-3.33

0.01

Since there is positive auto-correlation in the model, ARIMAX model is developed

The ACF and PACF plots are generated for the OLS residual

Based on the ACF and PACF plot, AR(1) model is developed

Reference: Time Series Modeling and Forecasting—An Application to Bank’s Stress Testing, SAS Global Forum 2015, Paper 3338-2015

ARIMAX model specifications

P, D, Q = 1, 0, 0

X = 3mT rate dyoy

When AR(2) term was introduced in the model, it was found to be insignificant, hence higher lags for AR are not included in the model

No. Obs:

44.00

AIC

1,380.03

Sample:

0.00

BIC

1,375.54

There are 2 variables in the model.

AR(1) term and 3mT rate (difference YoY)

The p-value for both the variables is less than 0.05

The sigma2 in the coefficients table is the estimate of the variance of the error term.

coef

std err

t

P>|t|

const

7,656,000.00

563,000.00

13.59

0.00

3mT rate dyoy

1,786,000.00

264,000.00

6.76

0.00

ar.L1

0.56

0.13

4.24

0.00

sigma2

1.75E+12

0.17

1.05E+13

0.00

It is observed that there is no auto-correlation in the model and the residual is stationary

DW test statistics is close to 2

The p-value of the ADF test is less than 0.10

Durbin-Watson:

1.77

Var:

ADF:

Pval:

RESI

-5.74

0.00

4.5 Projection

The projection is done for 13 Quarters

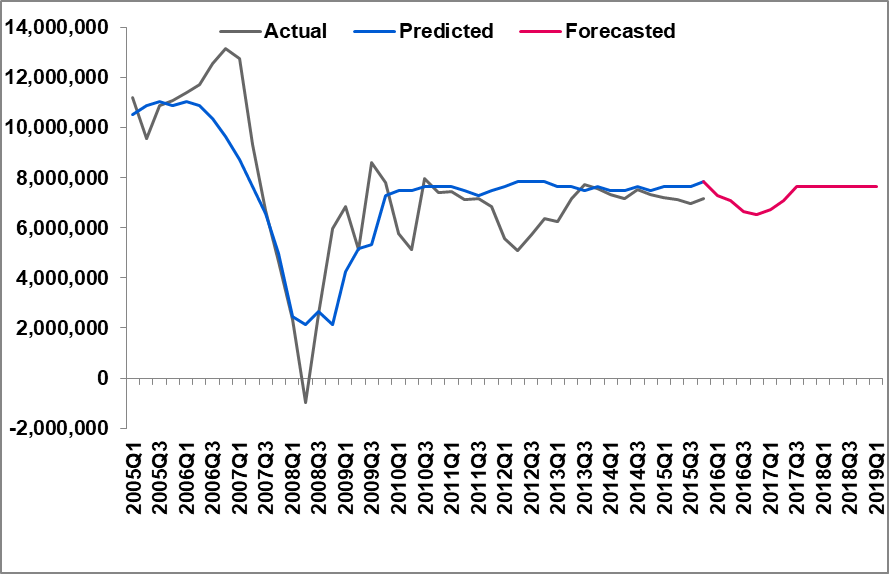

The dip in 2008-2009 is captured well by the model

The severely adverse projection is done for forecasted period